Clients, Colleagues, Partners, & Friends,

As the year draws to a close, I’m thrilled to present my First Annual Market Letter, an opportunity to reflect on the past year and share insights on the housing market, macro trends, crypto/AI, and predictions for 2025. Feel free to forward this to anyone who might find it valuable.

This year, my Team and I sold over $40M+ worth of properties, nearly sold out our New Development property, The Huxley, and took over sales at FIFTEEN at 15 W 96th Street. We are nearly sold out at Fifteen as we close out 2024 and expect to close out both New Development properties in 2025!

The biggest deal we closed in 2024 was just one day ago! We just closed #PH30A at 30 E 85th Street and the last asking price was $18.5M! This was one of the most challenging deals of my career and one that I will never forget since it taught me how to be relentless to get a deal over the finish line over the course of marketing this property over the past two years!

The highlight of my 2024 was watching Season 1 of Owning Manhattan air globally in over 170+ countries and become TOP 10 in 40 Countries. I’m thrilled to announce that Season 2 has already been renewed and we are currently in the midst of filming!

The real estate market has undergone significant changes, influenced by advancements in technology, evolving consumer expectations, and a dynamic economic landscape. AI, blockchain, and other emerging technologies are now as integral to conversations as classic real estate etrics like ROI and LTV. Navigating these shifts has underscored the importance of staying ahead of the curve and delivering value in innovative ways.

Looking ahead to 2025, I’m filled with optimism. This year was about laying the foundation, and next year promises even greater opportunities for growth and success.

Thank you for your continued trust and support. Your confidence means everything to me, and I look forward to building on our shared success in the year ahead.

- Nile

US Economic Update

The U.S. economy was defined by one major trend in 2024: The status of inflation. At the end of 2023, many expected that inflation would tame and the Fed would begin cutting interest rates in early 2024, but those rate cuts did not start until September due to unexpected market strength, which held inflation stubbornly above the Fed’s 2% target. The Fed made considerable progress, lowering inflation from its 40-year high of 9.1% down to 2.4% (see chart below). Now, the world watches on to determine whether the Fed waited too long or did too little to avoid tipping the U.S. into recession. At moments, that concern appeared well-founded – such as when employment numbers began to slip in early September – yet real GDP grew in each of the first three quarters and is expected to grow in Q4. This growth has been more moderate than in 2023, aiding inflation reduction. Business investment growth is down slightly from 2023 but still shows a healthy positive gain of 4.2%. Overall, the economy has shown an uncanny resilience in the face of high costs for just about everything, geopolitical conflict, and persistent economic uncertainty. We’ve seen this strength play out in the real estate markets, with nearly 70% of our firm's transactions this year being completed without financing.

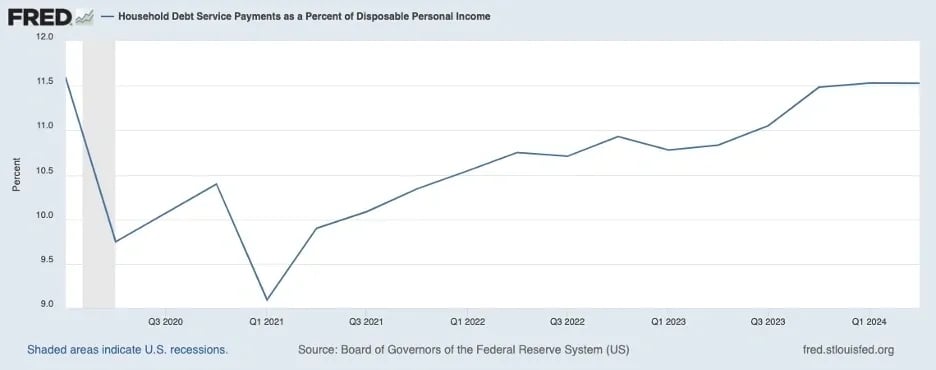

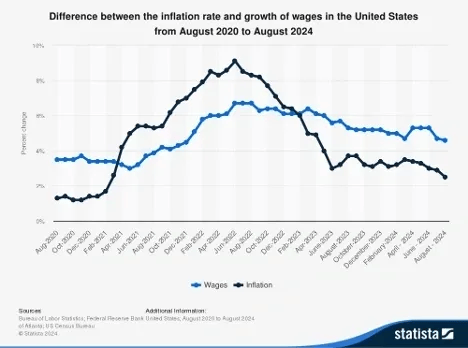

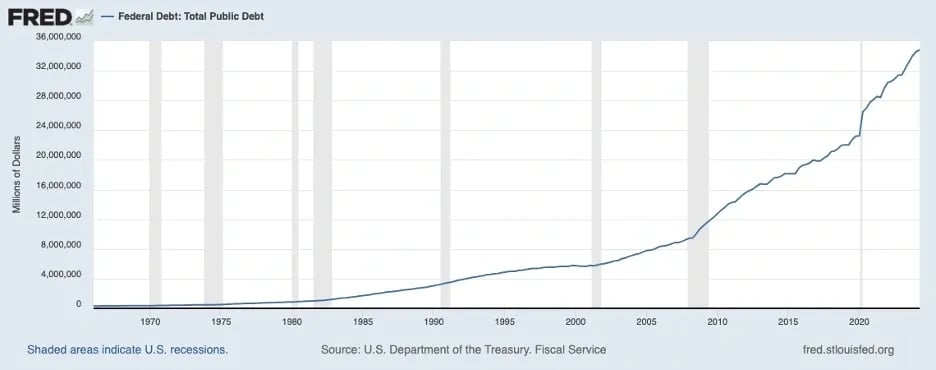

Still, while household balance sheets remain strong on average, debt balances have risen (see FRED Household Debt chart below), and delinquencies have increased YoY. Similarly, while overall labor participation remains strong and wages have increased (see Statista chart below), the number of job openings has decreased, unemployment has normalized upward slightly (see FRED Unemployment Rate chart below), and various industries were impacted unevenly this year. Government spending is ever-increasing, and while it’s lower this year than last due to some belt-tightening, the national debt is exponentially higher than ever (see FRED Federal Debt chart below). It may rise even more over the next four years due to new government expenditures and tax policy. There’s a new administration in town, and President Trump’s policies could juice the economy (great!) so much that inflation resurges (yikes!), and it will take severe national budget cuts and creative revenue increases to solve that problem and gain control of the deficit.

These factors remain items of concern as the Fed determines rate policy. Fed Chair Jerome Powell has committed to avoiding speculation and making calls on rates based only on facts. Cutting rates too soon or too fast could cause a resurgence of inflation, but not cutting them soon enough risks causing a recession. All in all, most economists and financial firms place the risk of recession in the next year at only around 25%, especially with Trump in office driving market stimulation. Investors agree. The stock market is a solid indicator of investor confidence in the continued economic strength of the U.S., and stocks are enjoying a glorious bull run. Still, what goes up eventually goes down, and because of geopolitical conflicts and trade policy issues, I am betting that there will likely be a severe market downturn between now and 2030. When that time comes, remember fortunes are often made during hard times.

Investment Markets

Markets have behaved strangely this year as the U.S. economy showed persistent strength in the face of inflation and high interest rates. Conflicting data impacted various markets differently, causing uniquely modern anomalies. One example is persistently high bond yields despite the Fed cutting interest rates three months in a row[1] | [2] . Now, the U.S. faces new contradictions as Trump promises to stimulate the economy but serves up policies that risk stoking inflation again. Below, I’ll discuss how different markets are reacting to this conflux of data and speculation.

Stocks

Stocks have been on a tear in 2024, repeatedly reaching record highs thanks to the thriving AI sector and tech stocks like the Magnificent 7. This culminated in the best day of the year, November 6th, after Donald Trump was elected 47th president of the United States. As of today, year-to-date, the S&P 500 is up around 28%, and the Dow Jones is up nearly 17%. With over 60% of Americans invested in stocks either directly or indirectly [Statista], this represents astronomical wealth growth amongst U.S. citizens. By many accounts, the ‘roaring 20s’ are set to continue through this decade with strong economic principles and productivity projections supporting ongoing company earnings, especially for small- and mid-cap stocks that benefit from an America-first environment.

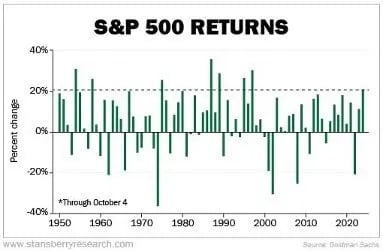

The chart below looks at S&P 500 returns since 1950. The index has only posted a better return than what we're seeing this year seven times in that 74-year span. And returns were positive the next year in six out of those seven instances. Take a look.

Of course, the market is not without its risks. Headwinds such as rising geopolitical conflict, resurging inflation, political uncertainty, and increases in debt default could change the tides. Non-U.S. stocks, for example, are taking a turn for the worse post-election on speculation of soon-to-come rising inflation in the U.S. and globally. If that inflation comes to pass, it will also challenge domestic stock growth.

We may see some volatility in the new year as new policy initiatives are introduced, uncertainty around them is digested, and consumer spending experiences the impacts of these various policies. But, historically, we are nowhere near the height of gains or the typical length of previous bull markets. Nothing lasts forever, but I predict that any notable downturn is still years away. The wealth accumulation this bull market has catalyzed will continue to make its way into real estate and SERHANT. has been busy managing the demand.

Bonds

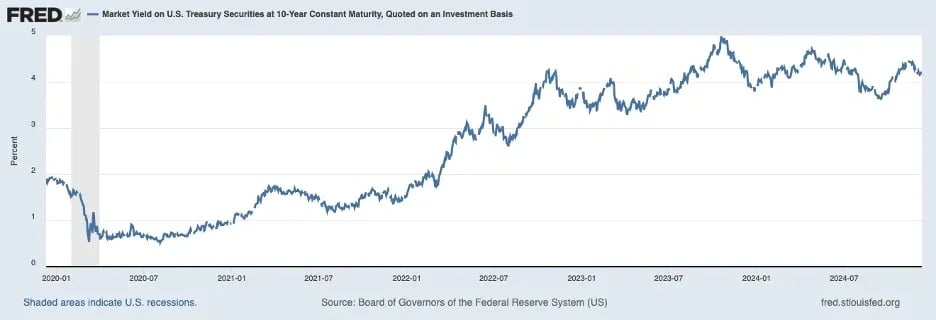

Bonds have been on a wild ride. After a record 793 days of yield-curve inversion, September 2024 marked the momentous occasion of the yield curve finally un-inverting. An inverted yield curve is a recession red flag, with a recession following every yield curve inversion since the 1970s [Statista], but despite the over 2-year inversion, the recession never came this time - at least not yet. The pandemic changed traditional economic wisdom, and this strange metric has abundantly clarified that.

Since the September curve normalization, the bond market saw yields on 10-year Treasury bonds spike by 21 basis points immediately following the election. They have since settled but are still higher than we saw throughout late summer and early fall. The spike was a reaction to the president-elect and his expected congress majority, causing concern for traders anticipating an increase in the deficit as taxes are cut and costly measures are tacked onto the government spending ledger. The Committee for a Responsible Federal Budget recently found that Trump’s economic policies could drive the national debt to as high as $7.5 trillion. Trump has proposed plans to combat inflation related to the national deficit, but the moves he’d like to make will be in Congress’ hands and will take time if they come to pass. This deficit risk seems to be the primary concern of bond traders, as this would cause inflationary pressure, to which the Fed would likely respond by pumping the brakes on their trajectory of rate easing or even new rate hikes. The bond market sent a message to Trump post-election to take it easy on tax cuts and expensive legislation or risk a significant rise in interest rates and hampered stock performance. Trump loves strong stock performance, so this dynamic might serve as a degree of checks and balances on some of the more costly legislation that Trump’s team has proposed.

Still, if the Fed is forced to hold rates high(er), could the yield curve invert again? If it did, would it be a harbinger of recession this time? What does this mean for mortgage rates?

I predict that today’s rate levels are here to stay through 2025, and we are working with our clients on creative options to lower their monthly payments. At many of our new developments, we are using sponsor financing and/or buy-downs to close deals.

Crypto

I’ve long shouted from the rooftops that Bitcoin was on its way to $100,000, and with roughly 140% growth since last year’s letter was published, we’re finally there! It feels so good to be right about this one, especially with one famous Million Dollar Listing New York clip from 2013 continuing to make the rounds! Even with crypto ETFs hitting the market in January, growth was steady through the winter and somewhat volatile throughout the middle of the year. But then we elected a crypto-friendly administration, and growth went through the roof, jumping nearly 30% following election day. But, we didn’t break the $100k mark until Paul Atkins was tapped as the new SEC chair on Dec. 4th. By that night, Bitcoin hit its highest price ever, just over $103,000 per coin. Even during the ‘Crypto Winter’ of 2022, I remained confident that regulation and legislation would strengthen crypto’s role in the market and help it become codified into the modern financial landscape. Paul Atkins is just the guy to lead this charge. Trump has promised to create a crypto-friendly regulatory environment, claiming the U.S. will become “the crypto capital of the planet” and that the U.S. would create a bitcoin strategic reserve to buoy national debt, and his decisions so far have lived up to the hype. The crypto markets have reacted with elation.

It’s not just Bitcoin, either. Ethereum, Dogecoin, Cronos, Neiro, and others have also seen staggering gains. Today, we’re seeing a resurgence of conversations with clients about crypto’s role in real estate transactions, and crypto ETFs are thriving.

The CoinDesk 20 captures the performance of top digital assets:

A few years ago, I said that 50% of all purchases would be in crypto. That was a bold prediction at the time, but the groundwork that’s being laid now is exactly what is needed to make that prophecy a reality. Crypto diehards: OUR TIME HAS COME!

Banking

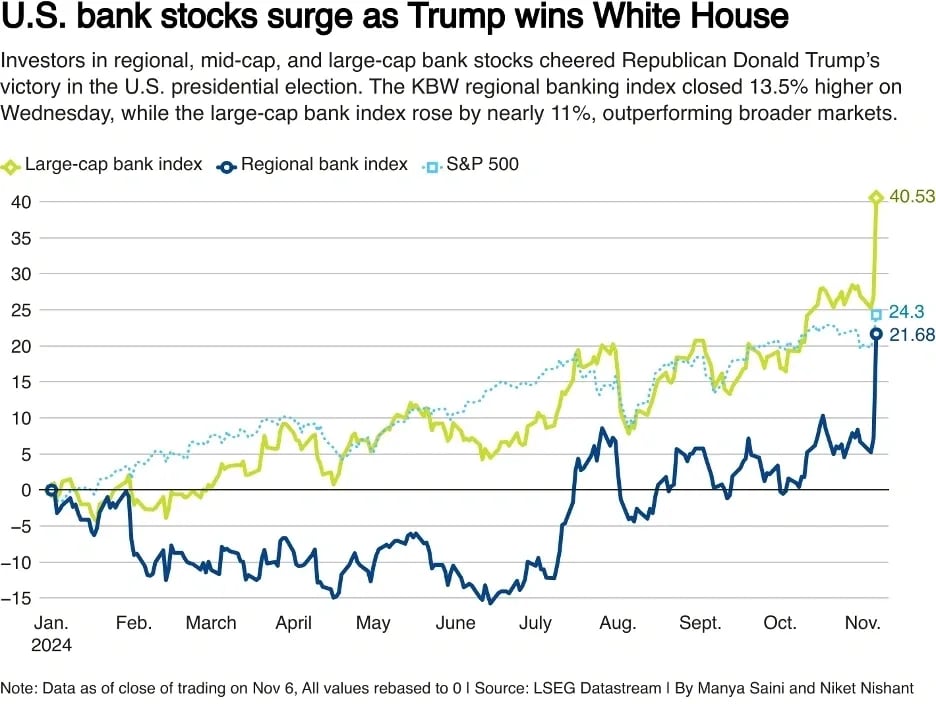

The newly-elected Trump administration is a promising windfall for the banking industry. As Christopher Marinac, director of research at Janney Montgomery Scott, told MarketWatch, he credits “a combination of regulatory relief and prospects for more business activity (i.e., more loans and deposits), which generates greater earnings.“ He added that even small increases in deposit and loan growth would boost banks’ earnings “incrementally.” On top of this could be “modestly lower tax rates” if the Republican Party achieves majority control of the House.” This lower-regulatory environment is expected to stimulate M&A activity that has been restricted by roadblocks that will now be cleared. I expect we’ll also see the end of discussions about the Basel III Endgame Rule, which would have increased banks’ capital holdings requirement to 9%, allowing that capital to strengthen banks’ bottom lines further. The market reflected its broad support of these expected policy shifts.

Via Reuters

The banking sector is not without its challenges, regardless of the current excitement. As unexpected consequences of new policies take shape, the possibility that international relations erode due to potential trade wars, and substantial inflationary pressures loom, there is good reason for the banking industry to stay on its toes. There is also growing competition from crypto markets and the fintech industry, low loan volume due to high rates, the loans held on struggling office space vulnerable to default, and an outsized share of low-interest loans held in our higher-rate environment. As with all markets, innumerable inputs can sway sentiment and cause positive and negative impacts. The banking sector is strong, but vigilance is critical.

Real Estate Industry Update

U.S. Housing Market

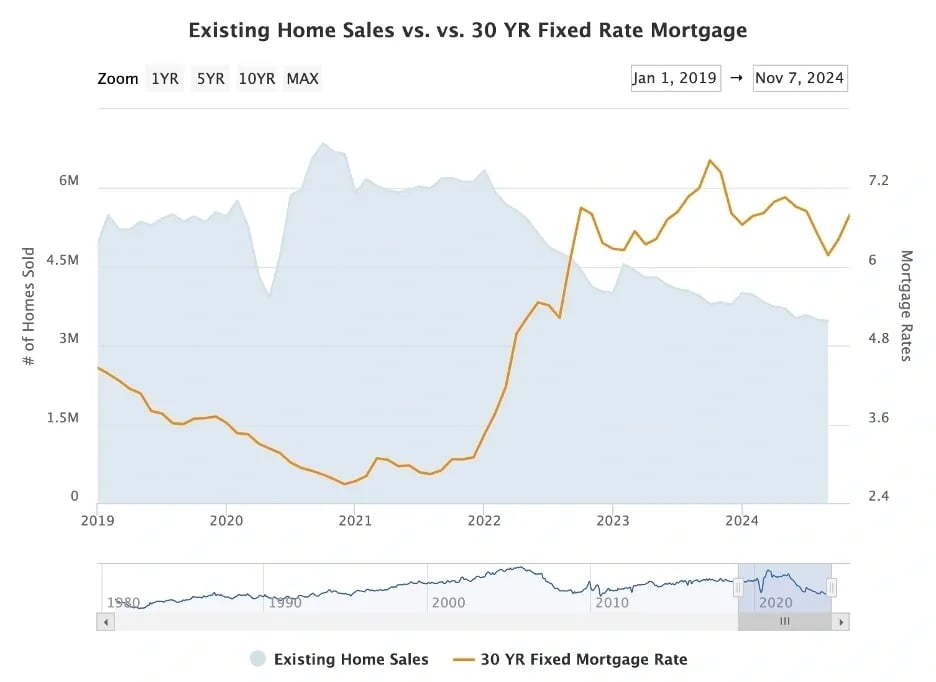

Nationally, 2024 will go down as the slowest housing market in over three decades. In 2022, real estate transactions ground to a halt as mortgage rates soared and affordable housing inventory remained constricted. 2023 brought the same challenges and an even slower market. In 2024, outside of luxury sectors, the US housing market sits in a place where Americans can’t afford to sell, and most would-be buyers can’t afford to buy, slowing the gears on any momentum we expected to catch coming into this year.

The reasons for low housing inventory are numerous. Chronic underbuilding since the great recession, the explosion in private equity, a population that is living longer than ever before, the mass movement that happened in 2020-2021 due to low interest rates and remote work trends, the ‘golden-handcuff’ effect (homeowners hold low mortgage rates and are hesitant to trade them in for higher ones when they move), and rapid price increases across the nation over the last five years. Low inventory is a long-term problem without a short-term solution. Agents were bemoaning low inventory long before the pandemic sent listings plummeting. While the market has experienced some slight easing of inventory woes due to highly restricted demand as of late, the U.S. is still short as many as 7.2 million homes, causing ever-rising home prices.

While mortgage rates were below 5% for the better part of the last two decades, even reaching as low as sub-3% in 2021, demand for home purchases surged. The imbalance between supply and demand during the pandemic caused home prices to explode – prices rose nearly 50% in the last five years on average. Then, as rates ratcheted up to 7-8%, demand cooled, and for the first time in a long time, we began to see more balance between supply and demand – but all at an extremely restricted level, leaving millions of Americans out of the market altogether. Mortgage rates began to decline in August but shot back up beginning in October, reaching 7.13% post-election [mortgagenewsdaily.com]. Rates are likely to experience greater volatility moving forward as markets shift due to evolving policy, destabilizing world events, and new inflationary pressures. After years in sellers' market territory, these factors have resulted in some relief for homebuyers, with a shift to a buyers’ market environment this year. Over the last two years, we’ve seen fewer bidding wars, homes spending more time on the market, and sellers increasingly willing to negotiate buyer-friendly contract provisions.

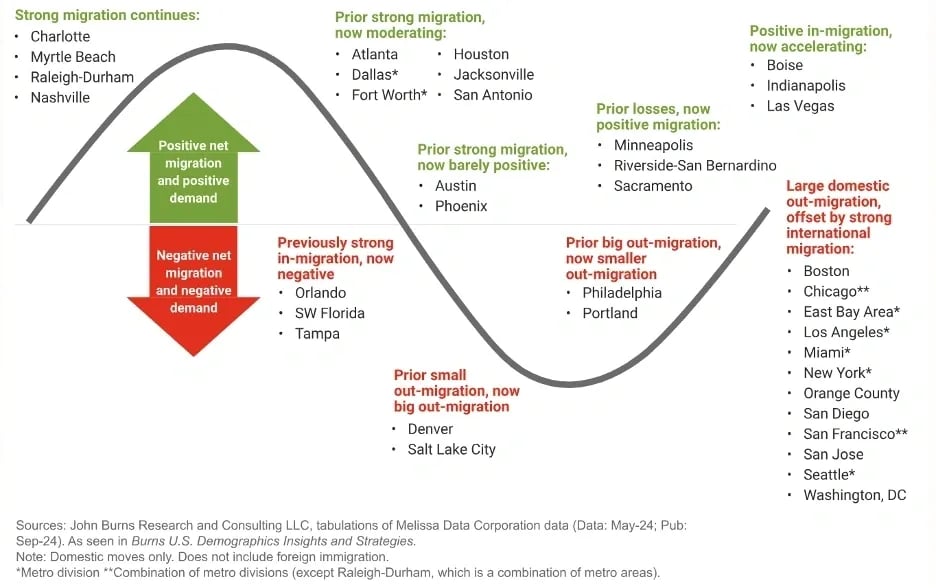

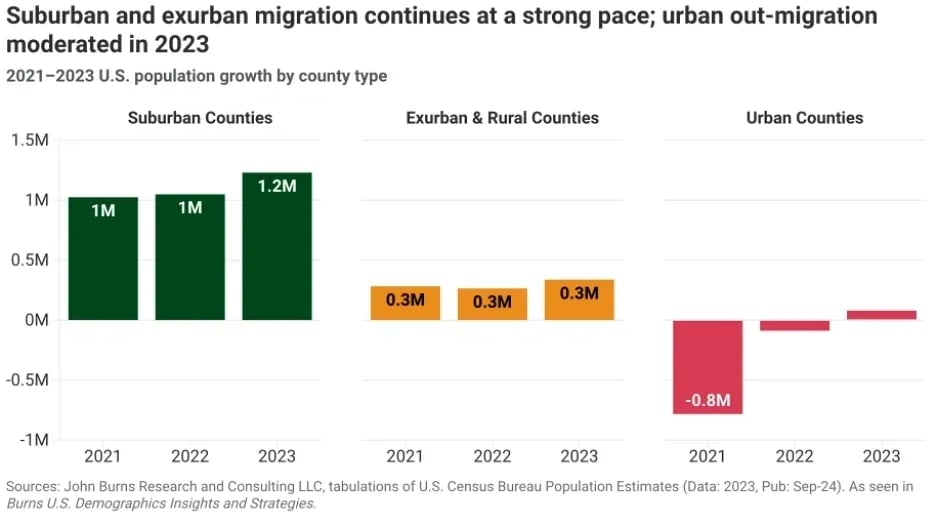

We’ve also seen the resurgence of regionality in market conditions. For a time during the Covid market frenzy, every area across the country saw skyrocketing prices more or less simultaneously. That wasn’t normal. Now, we’re seeing markets that surged during Covid experiencing challenges and markets that stayed more steady during those years experiencing continued stable growth. This is how it should work – geography, weather patterns, demographics, employment statistics, and zoning should influence various regions differently. This return to regional price dynamics represents a normalization in the market that we haven’t seen in many years.

Domestic Migration Landscape

Via PWC

As we enter 2025, there are many unknowns the real estate market will face. For one, it seems climate factors have begun to make a measurable impact on Americans’ housing decisions, prompting 1 in 7 households to investigate other places to live. Beyond the weather a certain locale offers, things like aging infrastructure and power grids, the likelihood of natural disasters, and costs like insurance and utilities are factoring into more peoples’ migration choices. Zillow will even add a climate risk score to every property in its database by the end of 2024. Additionally, building starts, mortgage rates, jobs, and wages are all extremely sensitive to policy and economic performance, and with a new presidential administration in town, the market trajectory is bound to shift.

That being said, if we stay the course, the path we’re on now will lead to more balance between buyers and sellers, lower rates over time, more moderate home price growth year over year, and increased affordability for homebuyers if wages continue to grow. In fact, NAR’s housing affordability index continues to improve. While this slow stabilization is a less flashy and exciting trajectory than the pandemic market offered, this more stable outlook is what both hopeful homebuyers and homeowners who would love to move need to reach their goals. I think this somewhat “boring” balance, while not without its pain points, is ultimately great news for the near future of the U.S. real estate market – a market where there is increased inventory, improving affordability, and more reasonable levels of competition. I don’t expect 2025 to be a wildly exciting year for the national real estate market (except at SERHANT.), but as many unknowns take shape this year, I expect the groundwork to be laid for exciting times in housing to come.

Luxury Markets

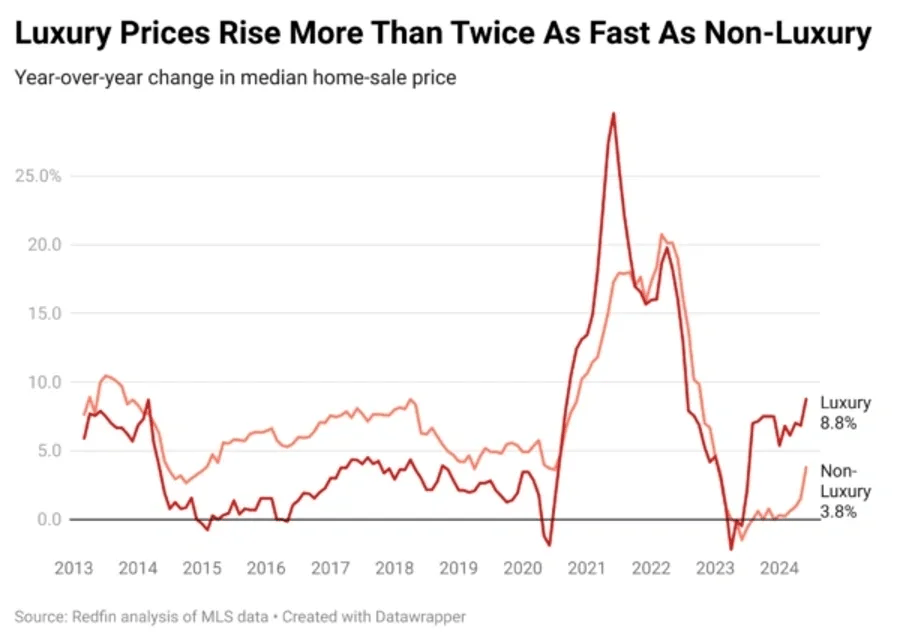

For several reasons, the luxury and ultra-luxury sectors of the real estate market behave differently than the more moderately-priced sector. Luxury homebuyers tend to be less rate-sensitive in their purchasing power, as nearly 45% of luxury homes are paid for all in cash. Additionally, high-net-worth individuals are benefitting from tremendous growth in personal wealth, which was realized thanks to strong stock performance this year. These homebuyers also enjoy the availability of financing options such as margin and portfolio loans and private bank loans. In fact, luxury real estate appreciated at 8.8% YoY on average across the U.S. as of the end of the second quarter. In comparison, the non-luxury market had appreciated only 3.8% YoY nationwide in that same timeframe.

The luxury market also tends to be highly location-dependent, with retiree destinations, vacation locales, and industry hubs showing greater strength on average than other markets. Realtor.com recently ranked the ten cities with the most significant price growth in their respective luxury markets, featuring places like West Palm Beach, FL, Reno, NV, East Hampton, NY, and Midland, TX. In NYC alone, we’ve seen a 9% increase in luxury ($4M+) and a 21% increase in ultra-luxury ($10M+) contracts YoY. But, even more noteworthy is the surge in luxury contracts we’re seeing at year-end – a stunning 46% increase YoY comparing September through December 12th, signaling a booming comeback after the sluggishness of 2022/2023.

While we are seeing continued strength in the luxury and ultra-luxury markets, 2024 has seen an increase in inventory and longer on-market times for these properties, reflecting an increasingly discerning buyer pool. The luxury sector does face some challenges: Strong stock market performance, such as what we see today, sometimes leads to restricted spending in areas such as real estate investment as investors resist paying capital gains to liquidate funds to allocate toward property. A strong U.S. dollar, like we’re currently experiencing post-election, can also restrict buyer activity from foreign investors, a significant buyer demographic in the luxury market.

Ultimately, homes that are impeccably presented and expertly marketed sell faster than the rest of the pack. For this reason, We provide white-glove branding packages for all our luxury listings and syndicate listings to more websites than any other brokerage, connecting with international and domestic high-net-worth portals in 80 countries. For luxury properties, SERHANT. Signature provides tailored, elevated service designed to showcase fine homes like no other real estate firm can.

Commission Lawsuit Outcome

The real estate industry experienced a shake-up this year as new rules regarding the handling of real estate agent commissions swept the nation. As a result of a lawsuit filed by former home sellers against NAR (The National Association of REALTORS®), which NAR agreed to settle, the industry has reshaped how commissions are negotiated and handled between real estate brokers and their clients.

In the past, when a homeowner decided to list their home for sale, they would negotiate the entire commission rate with the agent listing their home. That listing agent would then offer a commission split that they would share with the agent who brought the buyer to the table and facilitated the buyer’s end of the transaction. In other words, the seller paid the listing agent a commission, and the listing agent paid the buyer’s agent part of that commission. The NAR lawsuit deemed that practice unlawful. Now, the seller and their listing agent negotiate the commission paid to the listing agent, and the buyer and buyer’s agent have the option to negotiate the commission paid to the buyer’s agent separately. This change effectively means that a homebuyer is ultimately responsible for paying their agent out-of-pocket if necessary, potentially adding a substantial cost burden to homebuyers when housing affordability is already strained. Because of these affordability challenges, what happens most often is that homebuyers request in their offers on a home that the seller offer a credit at closing to cover their buyer’s agent’s commission, effectively rolling the commission into the purchase price of the house – which, by the way, is just a reengineering of how we’d always done it before.

So far, there has been little change or impact on the real estate market due to these new laws. In fact, in luxury markets, I’d argue that commissions have actually increased. It’s a hard metric to track, as commissions are not always public knowledge, but at SERHANT. we’ve seen increasing commissions to create competition for properties priced north of $10M. There is no reason to believe that market activity or buyer demand has decreased since these changes were enacted this past summer. As the market shifts, however, such as when more inventory hits the market, or we re-enter a scorching hot sellers' market, we will likely see a change in how buyers and sellers use commissions as a negotiation tactic. We could see buyers choosing to forgo using buyers’ agent services to save money, or they could use it to negotiate a better price. While there may be limited cases in which that would be a prudent strategy, it would expose the buyer to serious legal and financial risks and likely result in the listing agent receiving an increased commission that could compromise the buyer’s perceived savings without transparency. Seeing how these new laws play out in different market conditions will be interesting and may set new precedents over time.

The most significant changes we’re seeing thus far are in the paperwork and negotiation strategies the parties to a transaction must engage with. I spoke with CNBC when the lawsuit settlement was announced and went on the record to say that anything that increased transparency to the parties of a transaction – which these changes were intended to do – was a net win for the industry, a sentiment that I stand behind fervently. Unfortunately, I believe that the way the industry implemented these changes has resulted in greater complexity and more opacity to the detriment of the consumer. The contracts are more confusing, and the negotiations are more circuitous. We see that the best properties have never even been brought to the open market now, as the seller often has more to gain by selling off-market. These impacts contradict the lawsuit's intent and our desired outcome as industry insiders. Now, the Department of Justice (DOJ) is coming out against specific provisions of the settlement, saying they may stifle competition – to what effect is yet to be seen.

The lawsuits are not over yet. The next big lawsuit the real estate industry faces in 2025 addresses clear cooperation. This practice requires real estate agents to enter any home they list in the MLS (multiple listing service) database. The lawsuit alleges an antitrust violation and argues that home sellers should have a choice as to how they market their homes. Real estate agents argue that it is in the seller's best interest to have their home exposed to the most buyers possible and that the MLS and syndication services that pull their data from the MLS are the best way to accomplish this. Besides, contracts already allow sellers to exclude their homes from the MLS, and provisions exist that allow for ‘pocket listings.’ Like the commission lawsuit, I expect this will lead to diminished consumer clarity while exposing brokerages to greater liability and fewer protections for essential provisions such as commission and time-on-market opacity. The question that we, as real estate professionals, must ask ourselves is what should we do when the associations that govern us, associations of which we are paid members, expose us to greater liability and prevent us from representing our clients in the most ethical manner possible? At SERHANT., we consider ourselves incorruptible and will defend our agents and clients against anything that diminishes clarity or increases their expenses with the highest regard for dignity in business dealings.

President Trump 2.0—Analysis of Potential Real Estate Impacts

In November, the U.S. elected President Trump to serve his second (non-consecutive) term in the White House as the 47th President of the United States. Voters widely ranked the economy and high housing costs as top priorities in their voting decisions. While Mr. Trump and his team have yet to put forth detailed plans regarding their economic policies, much of his campaign was centered on these issues. Of course, campaign talking points aren’t always implemented as promised and can change dramatically once a President takes office and installs new people in positions of power. However, we can use these talking points to gain insight into how the Trump Administration thinks about the economy and housing market and the pathways they are exploring to address perceived problems.

I’ve identified the top six promises Trump made on the campaign trail that, if enacted, will likely impact real estate positively or negatively.

1. Tax Policy

Thanks to the Tax laws he signed into law in 2017, we already have quite a lot of insight into Trumpian tax policy, from reduced corporate taxes to caps on state and local taxes (SALT), removal of deduction caps, and advocacy for programs like 1031 exchanges and opportunity zones. We expect the incoming administration to extend and reenact these programs. While Trump’s ideas on tax policy vary in their impact by region, socioeconomic status, and more, the luxury and ultra-luxury real estate sectors benefit from many advantages under his tax code. The issue that Trump will face with implementing new tax cuts (beyond renewing the 2017 measures) is how they would impact the ballooning national debt. Without policies that would create new revenue (of which tariffs, as well as crypto investments, are two possibilities) and drastically cut spending (such as eliminating entitlements), new tax cuts may not be enacted as they could cause inflation and increased interest rates and could cause stock prices to lag – all of which would be hard on the economy and public perception of the administration if they came to pass.

2. Reduced Building Regulations

Eliminating red tape that increases the difficulty and cost of building new homes is a much-welcomed policy for most Americans and real estate industry professionals. The cost of a new home is estimated to have increased by $90,000 on average due to regulation expenses. While that number falls short of the 50% Trump posited that could be saved on the cost of a new home once building restrictions were eliminated, the savings would be monumental and allow for an increase in much-needed construction of residential properties across the U.S. The administration may see snags in this plan as many regulations they’d seek to relieve are in the jurisdiction of state and local governments. Still, red states and counties, in particular, stand to benefit from this plan. Democratic lawmakers have also supported decreased regulation for homebuilding as of late, so these measures have a good chance of passing.

3. Building on Federal Land

Another well-regarded policy amongst most Americans and real estate insiders is the plan to open up certain areas of federal land to construct new homes. I commented on this while in Dubai a few months ago, and you can read my thoughts in Arabian Business. These lands could see fewer building regulations, lower construction costs, and low property taxes. One downside of this plan is that there is little federal land available where most people work and live. Still, programs are being piloted that would allow for several federal agencies, including USPS and USDOT, to free up land for building in areas with housing shortages, and it is estimated that 1.9 million units near transit (though not necessarily populated areas) could be built nationwide. 1.9 million units would make a sizable dent in the U.S. housing shortage and be considered an indisputable win if it comes to fruition.

4. Deportation Efforts

Trump has pledged to implement “the largest deportation operation in American history,” arguing that, in part, this will ease demand for homes and rentals, thus bringing prices down. While there may be some truth to the concept that large immigrant populations in certain areas play a role in marginally increased demand for housing and slightly higher prices, the expected impact on housing prices due to this policy is minimal, in my opinion. Furthermore, this plan has short- and long-term risks that could drastically impact the real estate market.

For one, nearly 30% of the residential construction workforce is comprised of foreign-born workers (National Association of Home Builders), and many construction jobs already go unfilled. If the unemployment level were very high, this might not pose an issue as there would be plenty of U.S. citizens ready to step into the vacant positions; however, with unemployment at only 4% and a sustainably strong job market, no such pool of potential replacements for construction job vacancies exist. Deporting these workers could result in a massive slowdown of already minimal residential construction and increased construction costs, which would be passed onto the consumer.

Secondly, the cost of deportation of some 13 million immigrants would be deeply logistically complicated, unfathomably expensive, and would balloon the already astronomical national debt. As I previously mentioned, an increase in national debt would be a substantial inflationary pressure, and with inflation comes even higher mortgage rates – an obvious net negative for the real estate market.

Finally, the U.S. has a birth rate problem, with the current birth rate of 1.7 children per childbearing person sitting well below the rate of 2.1, which would be necessary to sustain the population. Immigration has offered the solution to this problem, as without immigration, the population would shrink. A declining population has many far-reaching catastrophic consequences and would reduce real estate demand such that house prices would plummet. One need look no further than China’s housing market problems for evidence of the havoc a declining population can wreak. If pathways for increased legal immigration are introduced and made accessible to those who wish to immigrate to the U.S., and policies emerge that support a higher birth rate, the fallout of tighter illegal immigration policies could be mitigated, but to what extent remains an important question.

For these reasons, it seems unlikely that mass deportation will occur as the risk of economic harm seems much more significant than any potential benefit. Instead, we can bet on stricter policies on illegal immigration, which would not have such a devastating impact on real estate.

5. Tariffs on Imported Goods

One of Trump’s more hotly contested policy proposals concerns imposing 60-100% tariffs on imports from China, 25-100% tariffs on imports from Mexico, and up to 20% tariffs on all other imports. The idea is to implement tariffs to decrease U.S. reliance on imported goods in favor of goods made in the U.S.A. In combination with other fiscal policy measures that increase revenue and lower costs, tariffs could help reduce the federal deficit; however, as a standalone policy, tariffs would be inflationary by increasing consumer costs. Inflation pressures could be reduced as the tariffs bring in revenue to offset the national debt. Still, they would need to be combined with other measures that could be divisive and would require Congress' approval to impact the economy for the better meaningfully.

The potential problems that the real estate market could suffer if these tariffs are imposed include increased construction costs of homes due to increased prices of imported construction materials and the possibility of higher mortgage rates if they prove to be inflationary.

6. Mortgage Rates

Trump has often promised that when he takes office, he will bring mortgage rates down to 2-3%, but it’s hard to imagine how he’d accomplish that, as the president has minimal control or impact on mortgage rates. Even the Fed, an independent nonpolitical federal agency that Trump has insisted he wants more control over, does not actually determine mortgage rates. Mortgage rates are determined by economic data and investors’ reactions to that data, and they closely follow 10-year Treasury bond yield trends. Investors are currently presuming that some of Trump’s policies will stoke inflation and increase the national deficit, sending T-bill yields higher despite the Fed’s recent interest rate cuts. This has sent mortgage rates higher in the wake of the election. As the new administration takes office, investor fears may be quelled, and rates could resume their decline. Regardless of the short-term impacts, volatility is expected during this presidential term as all three branches of the government have a conservative majority, allowing for changes to occur more rapidly than in previous years when there was more gridlock. After all, markets love gridlock as it offers assurance and slow change.

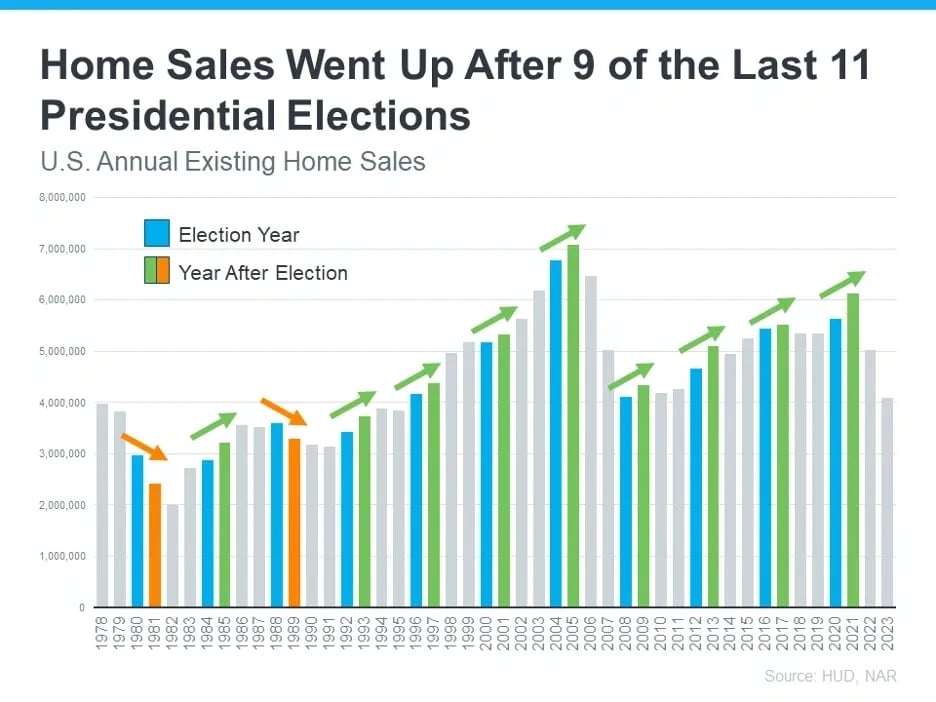

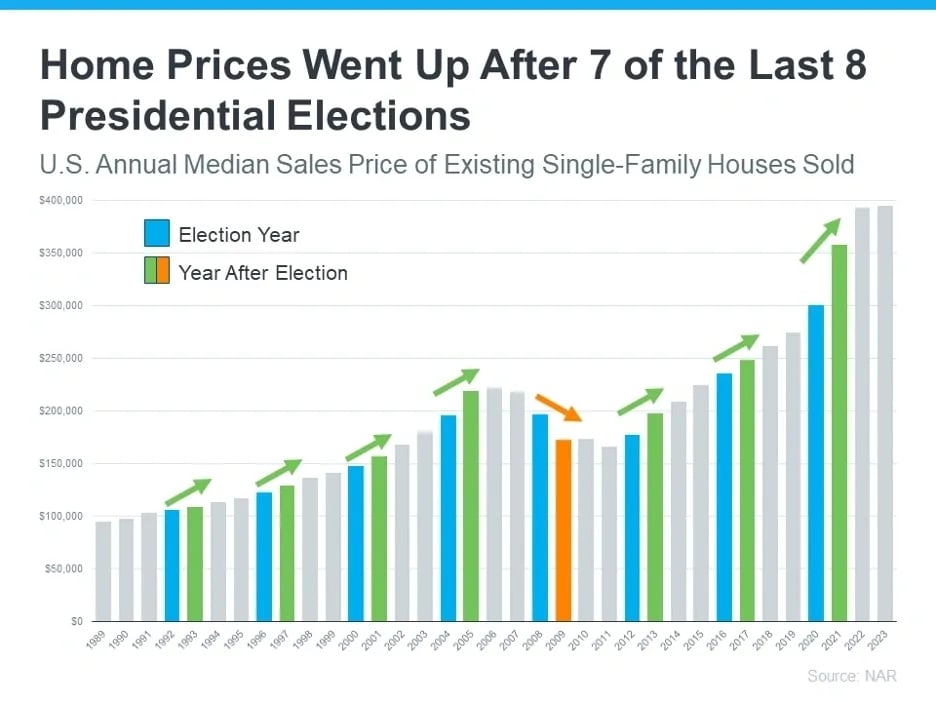

Despite these talking points, data supports that regardless of the outcome of a presidential election, the housing market typically sees a boost in the year following the election. In fact, in 9 out of the last 11 elections, home sales increased the year after the election, and in seven of the previous eight elections, home prices went up the following year. This could be attributed to slowdowns in the real estate market driven by consumer uncertainty in the months leading up to a major election, a new president’s determination to have a positive impact on their constituents' lives and the policy that supports that, or other random unrelated data – but the numbers don’t lie. For this reason and many others, I have faith that the 2025 housing market will show improvement over the 2023 and 2024 markets as we clear the way for a new administration, shake off the stagnant energy of the last few years, and pump the market with some fresh juice to fuel its next moves.

Automation Revolution

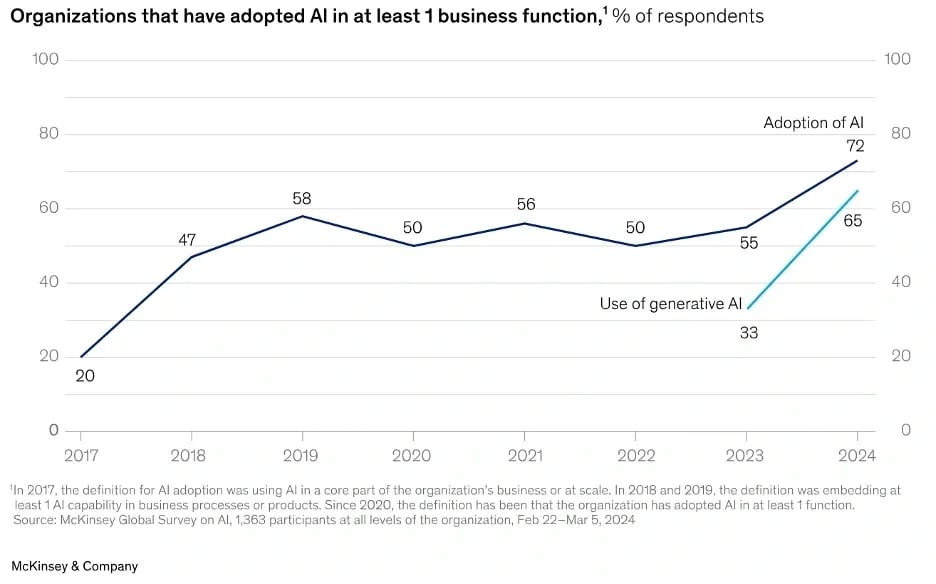

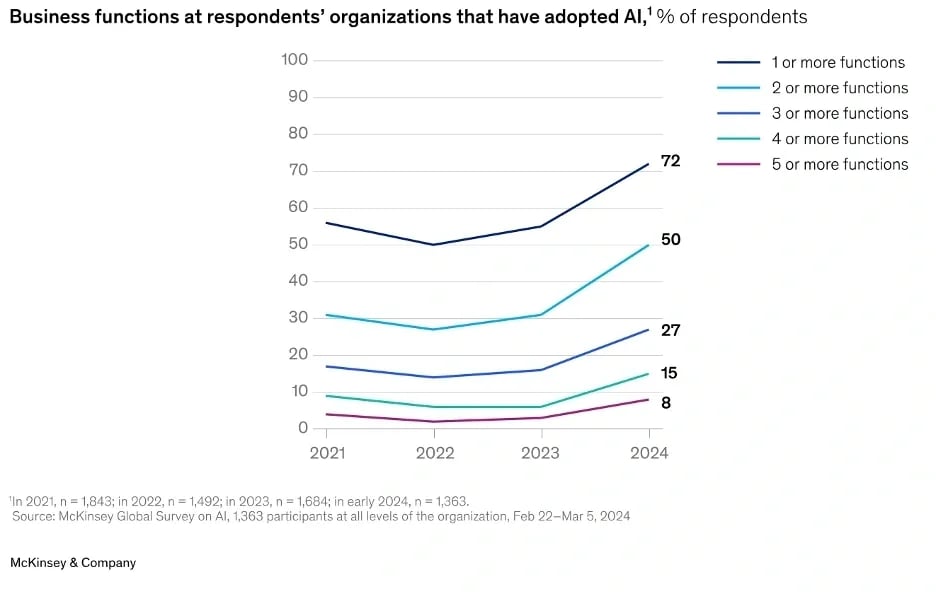

The adoption of automation and AI has exploded in 2024, with 72% of organizations now using AI in at least one business function, up from 50% last year. However, only 8% of organizations use AI in at least five business functions [McKinsey]. SERHANT. has embraced AI in every department, and I strongly believe that most organizations are getting it all wrong. Streamlining departments and increasing profit margins by reducing staff are features that AI offers, but the downside of companies that utilize this approach is that they become more robotic. They are drastically underutilizing and misunderstanding the breadth of the capability of these technologies’ ability to shift our peoples’ critical functions away from desks, behind screens, and back into the real world to create more human businesses, the way people have been craving since the beginning of the technological revolution.

Real estate is about to see an explosion in use cases of AI and blockchain frameworks as the incoming administration has declared extreme friendliness to crypto, as discussed earlier in this letter. There are now plans to put forth the first government regulation of any kind that will pave the way for more mainstream usefulness, adoption, and creative application not only of cryptocurrencies such as Bitcoin and Ethereum but of blockchain-based technologies writ large. It was always true that it was not possible to proceed with blockchain tech in this space until, as a society, we had the benefit of more time to analyze the space and until regulators began introducing and passing legislation on the topic that put a framework in place in which commerce could operate. That will likely happen now, which has made my prediction more possible, even if it hasn't come true yet. The AI revolution has caused a mega boom in the connected technologies space, specifically regarding LLM and LAM-connected platforms intertwined via APIs, that will intensify as agentic AI frameworks continue to gain momentum. We're seeing transaction management tools and companies begin to shift to a microservices architecture that allows for anything that can be done with a mouse and keyboard to be done via API by a bot or instruction set that can be passed through, or both. This fundamental change within the transaction management space lays the groundwork for more straightforward integration with blockchain-based conveniences and protections.

Leveraging emergent technologies has been central to SERHANT.’s mission since the inception, but in 2024, SERHANT. has took their biggest leap forward yet, launching an AI-backed tool that has changed how we work and given us more time to live. Because SERHANT. has a first-mover advantage in the automation space; we’ve had the opportunity to experiment, fail, and learn from those failures as we introduced AI-leveraged tools to our people while everyone else was still trying to figure out what AI is. The problem we came up against over and over was adoption. No one wanted to have to master being an AI operator. No one wanted yet another program, yet another screen they had to learn to use and incorporate into their daily lives. People are not longing for more tech to incorporate into their lives but rather for their lives to become easier, more connected, and more HUMAN. Herein lies the problem that every organization in the world will face as they incorporate AI and automation into their practices.

SERHANT. has long believed that we must build our tech to allow anyone to work from anywhere on any device. That philosophy has evolved to include the idea that we must also reduce screen time and the number of platforms our people need to interact with throughout their day and empower them to spend their time in the real, physical world with other people.

This year, SERHNAT. has launched the culmination of work in this space: S.MPLE. S.MPLE is the best Large Action Model to have ever existed (in my humble opinion) and the first one to ever hit the real estate industry. S.MPLE combines SaaS and human expertise to create what can be imagined as a digital factory assembly line that can take over the administrative tasks of salespeople and teams—ranging from marketing to client follow-ups and transaction coordination. Simply put, S.MPLE frees agents to focus on selling. Since launching, S.MPLE has processed close to 2,500 requests, saving agents more than 5,000+ hours by allowing them to manage their entire operations using only their voice–and that was just while we were in beta testing. Today, S.MPLE can perform 20 complex tasks or ‘Recipes’ that used to take agents hours in a matter of moments. And with every input, S.MPLE gets stronger, smarter, faster, more customized, and more capable of performing innumerable tasks. Selling and buying real estate just became a whole lot more S.MPLE, only at SERHANT.

Lundgren Team Business Update

2024 has been an extraordinary year for the Lundgren Team, marked by growth, excitement, and incredible accomplishments. We welcomed three talented new members to our team, bringing fresh energy and ideas to our projects.

This year, we proudly sold several remarkable properties, including 30 East 18th Street, 515 East 72nd Street 5J, 331 West 18th Street, and 96 Bank Street. These sales represent our continued commitment to excellence and our ability to deliver results for our clients across the city.

The debut of Owning Manhattan on Netflix in June has been another thrilling highlight. The show has captivated audiences worldwide and showcased the vibrancy and challenges of Manhattan’s real estate market.

We’ve also been fortunate to gain recognition across a variety of prestigious media outlets, including The New York Post, Koimoi, House Beautiful, SportsKeeda, Meaww Official, The Cinemaholic, Vogue, HousingWire, Cottages & Gardens, Real Tea, and NBC. These features have amplified our story and underscored our position as leaders in the industry.

Additionally, we’ve had the privilege of sharing our expertise at various events and on multiple podcasts, including The Broker That Never Sleeps. These opportunities have allowed us to connect with industry peers and share insights about the ever-evolving real estate market.

As we look ahead to 2025, we’re excited to build on this momentum, tackle new opportunities, and continue to make an impact. Thank you to everyone who has supported us on this journey—it’s only the beginning!

New Development

Our new development team knocked it out of the park this year with $4B in inventory and nearly 50 projects in total for 2024, and even won the “Best Sales and Marketing Campaign for New Development 2024” by Inman’s Golden Club for Mercedes-Benz Places in Miami. Our New Dev team has been relentless in their efforts to scale and innovate, which has attracted unparalleled attention and record-breaking deals for our developer clients.

Among our 2024 wins are the following:

One Williamsburg Wharf

- Within the first month, we achieved an impressive milestone: 30% of units were sold

Mercedes-Benz Places in Miami

- Awarded nationally as the “Best sales and Marketing Campaign for New Development 2024” by Inman’s Golden Club

- Sold 100 units in under 5 days

200 Amsterdam

- Since taking over the project, we have increased traffic by over 150%

- Over $18M in contract in November of 2024—blending at $3,460psf.

Fifteen Off-the-Park

- Almost sold-out of all the units!

Conclusion

As we close 2024, I’m incredibly proud of what the Lundgren Team has accomplished. From welcoming new members and selling standout properties like 30 East 18th Street and 96 Bank Street to the successful premiere of Owning Manhattan on Netflix, this year has been monumental.

We’ve been featured in top outlets like The New York Post, Vogue, and NBC, and shared insights at events and on podcasts like The Broker That Never Sleeps. These milestones reflect our dedication to excellence and innovation in real estate.

Looking ahead to 2025, I’m excited to build on this momentum. With a growing team, bold strategies, and the trust of our clients, we’re ready to make the new year even more extraordinary.

Thank you for your continued support—wishing you Happy Holidays and a successful New Year!